- Renewables Rising

- Posts

- Private equity fund EAAIF raises $325m in debt

Private equity fund EAAIF raises $325m in debt

From the newsletter

The Emerging Africa & Asia Infrastructure Fund (EAAIF), a private equity fund, has completed a $325 million debt raise for investment in infrastructure projects including clean energy across emerging markets. This latest funding round brings EAAIF's total recent capital raised to $620 million, surpassing its initial target of $500 million by the end of 2025.

About 21 African governments are either at high risk of debt distress or already in debt distress, which limits their investments in energy. Estimates suggest $190 billion is needed annually until 2030 for energy transition goals.

Private equity (PE) players are angling for a share of this market. Several funds have been raised to support renewables investments. Evolution III fund recently raised $238 million.

More details

EAAIF is managed by Ninety One and a Private Infrastructure Development Group (PIDG) company. It has now raised over $1 billion in commitments since 2018 as it plans to deploy it into critical infrastructure projects in Africa and Asia by 2028, focusing on digital economies, transition infrastructure, and reshaping power markets.

The funding was led by Allianz Global Investors, committing $113 million, with contributions from ABSA ($75 million), Standard Bank ($50 million), Sumitomo Mitsui Banking Corporation (SMBC) ($50 million), and Swedfund ($45 million). This broad support from global public and private investors signals confidence from investors in their work.

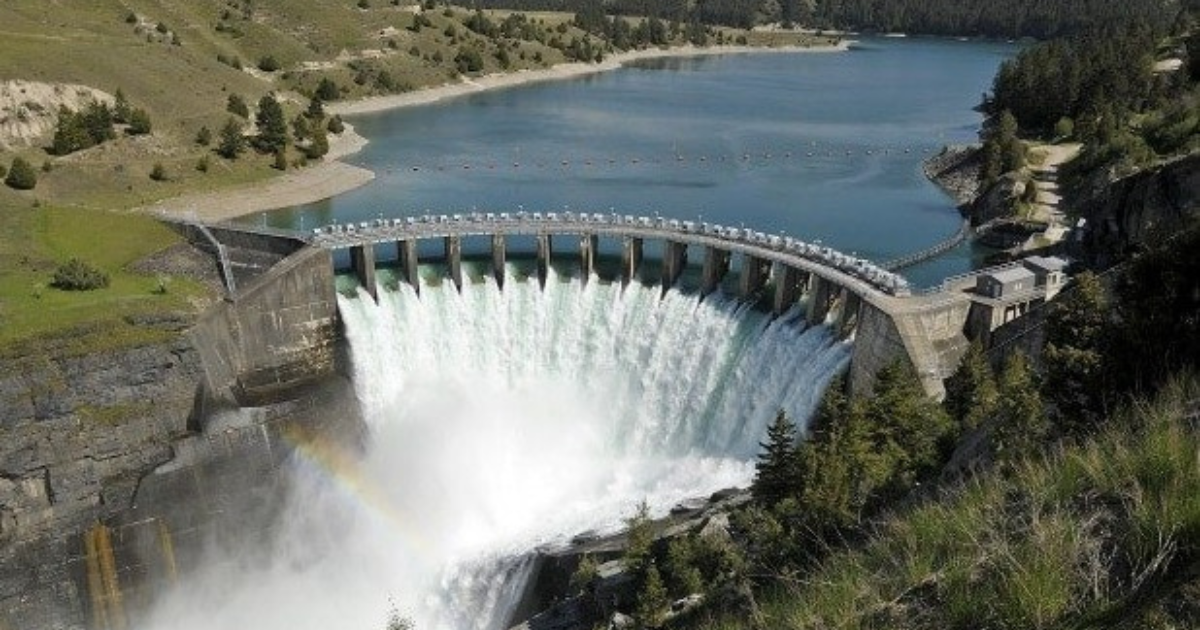

The fund invests directly in projects or companies in renewable energy across African and Asian emerging markets. In Africa, it has invested over $200 million. It recently invested $45 million in CrossBoundary Energy and last year invested $40 million in Hassan Allam Utilities to fund its pipeline of projects in Egypt. It has also directly invested in projects, including a $32 million solar plant in Côte d'Ivoire and $23 million for a 35 MW hydropower plant in Gabon (Pictured).

Multiple funds have entered the market in the wake of renewed electrification efforts by the World Bank and AfDB. Many countries have improved their policy space and aligned it with energy transition goals. Some of the main private equity companies include Africa50, which plans to raise $500 million and Cape Town-based Inspired Evolution, which runs Evolution Fund III and aims to raise $400 million. So far, it has raised more than half of this.

Investments in the renewable energy space are becoming attractive as the technology matures and prices decline. This, coupled with demand, directly improves project economics, making projects more attractive to PE funds seeking competitive returns.

The ability to deploy smaller, modular, and decentralised solutions (mini-grids, C&I solar) reduces the scale of individual project risk. This allows private equity to target a wider range of projects and customer segments that were previously inaccessible markets, such as rural communities and specific industrial clients that are not served by central grids. This is creating new investment opportunities for PE that are less reliant on large-scale, politically sensitive infrastructure projects.

Our take

Africa's demand for renewables will continue to grow, but this growth will not be uniform. Some countries will offer greater potential. Funds should target high-return markets. South Africa, Egypt, and Morocco have significant consumption demands that can guarantee revenue in well-structured deals.

However, investors must exercise caution during due diligence. The risk profile, especially the political one, is substantially high in many countries where policies change with different regimes.

As more private equity players enter the market, those that secure their funding cheaply will be better positioned to compete. Such funds should aim to source a mix of concessional loans from development finance institutions to reduce their cost of lending.